Inflation is the economic word of the year. The most recent Consumer Price Index showed prices climbing 8.6% in May 2022. That’s the fastest rate of inflation growth in 40 years.

Kind of a big deal.

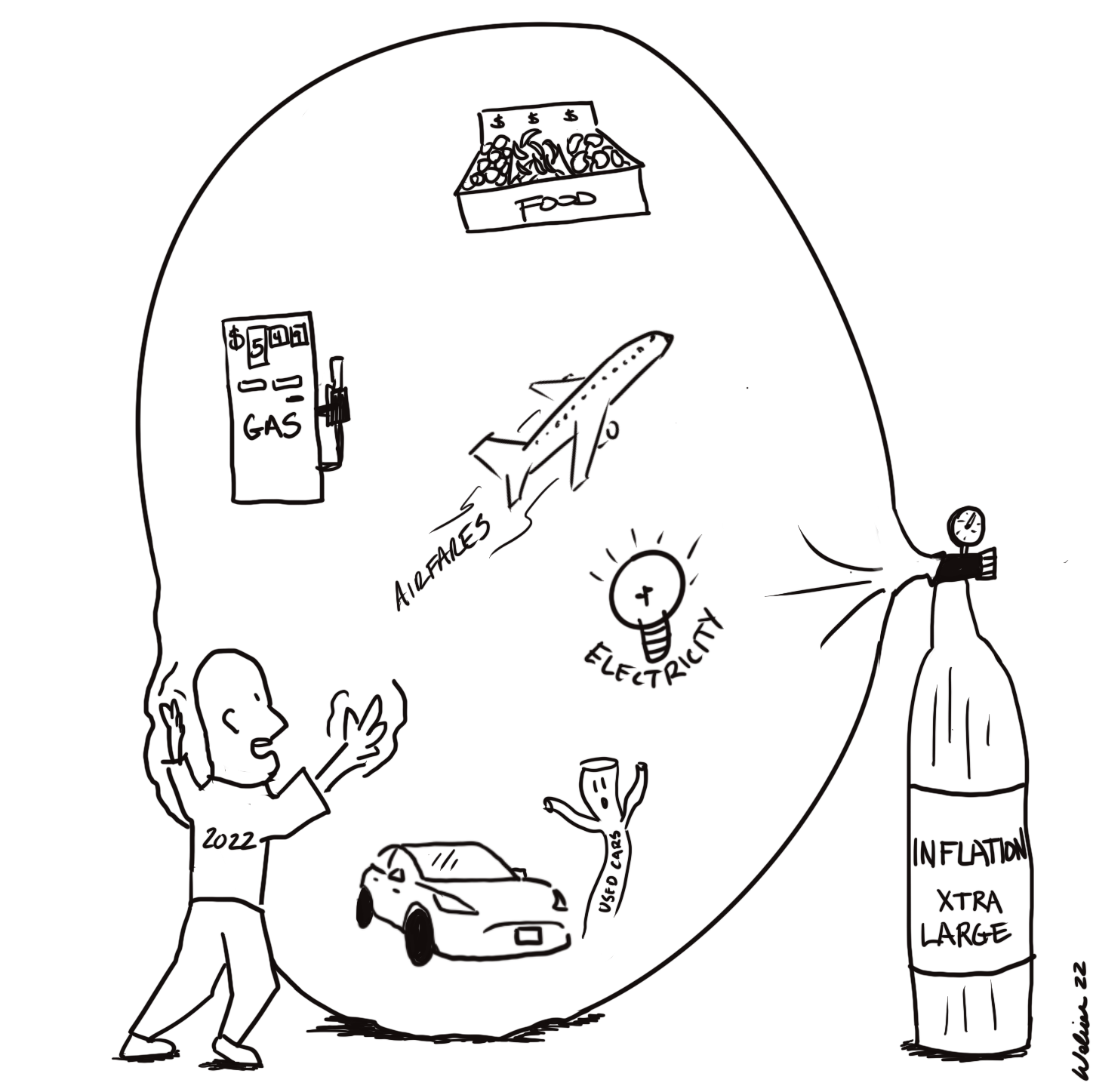

How inflation affects us

Everything costs more than it did a year ago. Some things more than others (cars, gasoline, food). You don’t have to be an economist to understand that prices can’t rise this quickly for long before there’s a real problem on our hands.

High inflation means our paychecks and our savings accounts buy less than they used to. If it goes on long enough, individuals and companies stretch their dollars by buying less. When everyone buys less, the economy shrinks and we experience a recession.

We may be past the point of no return, meaning a recession is imminent.

Personally, I’m in a flexible early retirement situation (call it F.I.R.E. if you must). This means that I rely upon withdrawals from my investments to fund a part of my living expenses. Seeing both high inflation and a falling stock market, I’m sharpening my budgeting pencil. Big expenditures are going on hold. Next winter’s vacation plans will be scaled back. I’m becoming more deliberate with routine purchases to ensure I’m getting the best deal.

I’m blessed with ample financial means. If I’m taking these steps, you can bet a majority of Americans are, too. As should you.

Why we have high inflation

Inflation shouldn’t be a surprise.

Some inflation is a normal and expected part of a normal economy. Policymakers try to keep average annual inflation around 2%. They do this by adjusting interest rates. When inflation is low, they lower interest rates to make it cheaper for people to borrow and spend money. When inflation is high, they raise interest rates to discourage borrowing and spending. It’s a balancing act. Raising interest rates too high can cause a recession just as quickly as high inflation.

Here’s the thing: Until recently, inflation has averaged even less than 2 percent for two decades. For Millennials like me, this is the first time in our adult lives we’ve experienced high inflation.

Why now?

There’s never one single thing that causes inflation. Even economists can have a tough time pinpointing the reasons why inflation ebbs and flows. This year, however, we know there are a few key factors at play:

- Too much “printed money” in recent years (tax credits, stimulus packages, bond buy-backs)

- Pent-up consumer demand following COVID

- Supply-chain issues and commodity shortages (e.g., shipping delays, semiconductor shortages)

- The war in Ukraine creating shortages of oil and food

The truth is, any one of these factors could cause an uptick in inflation. So it’s not surprising that, together, they’re causing the issues we’re seeing now.

Planning for inflation

During my years publishing Money Under 30, I wrote about the importance of inflation in long-term planning and investing. Sometimes, I sounded like a broken record. Because I knew this day would come.

Inflation is the reason you can’t just keep savings in cash or in a basic savings account over the long-run. Every year that passes, a dollar is worth a little bit less. Many years it might only lose a penny or two in buying power. Then you get year like 2022. It’s only June, and a dollar you got a year ago is already only worth about 92 cents.

Inflation underscores the importance of investing in assets with the potential to significantly appreciate over time.

The math is simple. If inflation averages 3% and your stock portfolio provides and average annual return of 7%, the real value of your money will grow by 4% per year. Conversely, if you held that money in a savings account paying 1%, the value of your money would decline by 2% per year.

Real (inflation-adjusted) returns on $10,000, 3% average inflation

| $10k invested at 7% | $10k saved at 1% | |

| 1 Year | $10,386 | $9,709 |

| 5 Years | $12,025 | $9,057 |

| 10 Years | $14,212 | $8,185 |

| 20 Years | $21,426 | $6,644 |

| 30 Years | $31,361 | $5,240 |

| 40 Years | $40,799 | $4,564 |

Living with high inflation

Investing is the only way to protect your assets against the inevitable inflationary erosion of their value. But what do we do when living through high inflation, as we are now?

Two things: Buy less and use debt strategically.

Common sense dictates that higher prices will naturally lead most of us to buy less. Often, it just has to be that way. We only have so many dollars to spend. If more of those dollars are going to fill our gas tanks and grocery carts, there are fewer left to spend on everything else. Taking a proactive approach to tweaking your budget will give you more control over how inflation (and a potential recession) affects you and your family.

What’s also interesting is that it can be smart to borrow money when inflation is high.

If you know me, you know that I’m conservative about debt. I always recommend steering clear of credit card and personal loan debt. That doesn’t change.

Paying cash for cars and paying off a mortgage early have also been things I’ve recommended for many consumers. There are always trade-offs. But in recent decades of low inflation, the benefits of being debt-free had an edge on the benefits of using credit to leverage your ability to invest.

High inflation changes the equation.

Let’s assume inflation continues at 8% for another year. (Although I hope not!)

Before interest, a dollar borrowed today will only be worth 92 cents a year from now. In real terms, you get a dollar today but get to pay back less than a dollar.

Of course, this why banks change interest. But when you can borrow money for less than the prevailing inflation rate, you stand to gain. (Just like when you invest in assets that appreciate faster than inflation.)

As I write this, the national average interest rate for a 48-month new car loan is 4.50%. That’s 3.5% less than the prevailing inflation rate. This makes it financially advantageous to finance a car rather than pay cash.

Mortgages work the same way.

Interest rates are on the rise, however. If inflation stays high, policymakers will continue to raise interest rates. Eventually, rates and inflation could approach an equilibrium, again reducing the incentive to borrow.

When will high inflation end?

Your guess is as good as mine.

Sustained high inflation is political kryptonite, so you can bet the Biden administration is desperate to put an end to it. The question is whether or not they can.

Most likely, it will take a recession. Not that I would, but if I had to bet on it I’d say that recession is forming now, in the middle of 2022. Perhaps it will hold off a few more quarters.

Barring anything extreme, I think an “average” recession would actually be a good thing for the world. A reset in housing prices would benefit buyers. Reduced consumer spending would take some pressure off of supply chains and a labor market that’s making it impossible for businesses to stay fully-staffed and, at least where I live, open normal hours.

What we don’t want is for a recession to come on and then high inflation to persist. Then we get stagflation — high inflation combined with negative or zero economic growth (stagnation). It happened in the 1970s, and it’s ugly because it means investors will not earn a positive real rate of return for many years.

With any luck, we’ll have a mild recession, inflation will ease, war will end in Ukraine, and better times lie ahead. Here’s hoping.

The takeaway

Inflation scares me, and it should scare you, too. It’s the economic boogeyman. Recessions come and go as a part of normal economic cycles. But inflation can be a wildcard. (See the 1970s, when inflation rate above 5% and, at times, above 10%, for more than a decade.)

Inflation makes everything more expensive. That makes it harder to get ahead. If you can get ahead and start saving, inflation then makes it harder to earn real growth on your investments.

The golden rule of money is to “spend less than you earn and invest the difference”. Inflation doesn’t alter that rule, it just emphasizes its importance.